Rate hikes to follow the Fed would work. But the Bank of Japan continues to dig its heels in. However, its balance sheet has been dwindling for months.

By Wolf Richter for WOLF STREET.

The Bank of Japan is now seriously considering supporting the yen with direct market intervention, after government and BoJ maneuvers failed to stem the yen’s slide against the dollar.

The BoJ conducted an “exchange rate check” on Wednesday, asking market participants about trends in the forex market, according to sources cited by the Nikkei. “This is believed to be a move to prepare for a currency intervention,” said the Nikkei said.

The yen began to dive against the dollar in January 2021. Back then, it took around ¥104 to buy $1. The fall accelerated in March 2022, when the Fed began to raise its key rates. Last night it took ¥144.8 to buy 1 dollar, a level the yen hasn’t seen in decades. On news of the rate control, the exchange rate briefly rose ¥2 to ¥142.7, but has already given up some of the gains and is trading at ¥143.2 against the USD, while the markets feed their doubts,

If the Treasury and the BoJ really intervened, they would have to sell foreign currency assets, such as holdings of US Treasury securities, and buy yen with these dollar receipts.

But intervention is limited by the amount of foreign exchange reserves Japan has, and it cannot be the kind of unlimited “whatever it takes forever” threat that central banks like to pose to countries. markets.

And the markets know it too. And that’s why supporting a currency by selling limited currency assets might slow short-term decline, but is not a long-term solution to a collapsing currency.

For the US, Japan’s currency sales also present an interesting aspect: if these sales are large enough, they will put downward pressure on prices and upward pressure on yields.

Finance Minister Shunichi Suzuki told reporters today that there would be no pre-announcement of an intervention and authorities would not usually confirm afterwards that an intervention had even taken place , according Reuters. “If we had to intervene, we would do it quickly without any interruptions,” Suzuki told reporters.

The fall of the yen against the dollar is a big problem for Japan that the authorities have been deploring for months: Raw materials, fuels (almost all of which are imported by Japan), agricultural products, industrial materials and components, consumer goods , etc., are becoming much more expensive to buy with the much weaker yen, which has squeezed profit margins, inflated the trade deficit, and fueled the wrong kind of inflation that is reducing consumer consumption.

The weak yen, which exacerbates soaring fuel prices for Japan, triggered a massive wave of monthly trade deficits from mid-2021.

The Ministry of Finance has already contacted the US Treasury Department and requested a coordinated purchase of yen to support the currency, but was rejected, Japanese media reported in April. So unilateral intervention now with limited foreign exchange reserves would be all Japan can do.

Everyone knows what the problem is.

The Bank of Japan has not moved from its negative interest rate policy for short-term interest rates and it is still holding its fixed 10-year rate of return below the 0.25% it threatens to apply with “unlimited” purchases from the Japanese government. Bonds (JGB), even though inflation in Japan has exceeded its target, and even though the Fed, ECB and other central banks have raised their rates by significant increments.

The BoJ could solve the currency problem by dropping its rate peg to the 10-year yield and letting it go, and raising its short-term policy rates in big catch-up rate hikes to approach rates of the Fed, and increasing quantitative tightening.

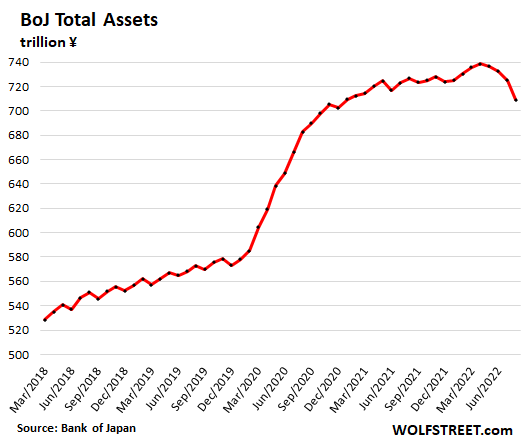

But BoJ Governor Haruhiko Kuroda, a remnant of Abenomics that relied on a huge burst of money printing and interest rate repression, will remain in office until April 2023, and he is hooked on rate hikes.

It has already ended the money-printing spree for which Abenomics became infamous, and the toll has been falling for four months. But rate hikes, ouch! Not Kuroda. He always talks tough and blows businesses frustrated with soaring costs and consumers frustrated with rising prices.

Do you like to read WOLF STREET and want to support it? You use ad blockers – I completely understand why – but you want to support the site? You can donate. I greatly appreciate it. Click on the mug of beer and iced tea to find out how:

Would you like to be notified by e-mail when WOLF STREET publishes a new article? Register here.

![]()